“Heterogeneous Effects of the Credit Environment on Entrepreneurial Entry” [Paper] [Code] [Slides] – Job Market Paper

Abstract

Startups are vital to the economy, driving job creation, innovation, and competition. A major barrier to entrepreneurship for households is a lack of funds. Credit-constrained households are more likely to start businesses when these constraints are relaxed, either through increased wealth or a loosening of the credit environment. This paper uses G-estimation to examine how changes in wealth and the credit environment influence households’ entrepreneurial entry, particularly during the COVID-19 period’s boom in new business applications. The method disentangles the impacts of wealth and credit environment shocks, analyzing heterogeneous effects based on different wealth sources and levels. I find that credit tightening amplifies the influence of wealth growth on entrepreneurial entry. Specifically, households receiving lump-sum transfers are more sensitive to credit tightening, with each 1% increase in credit tightening amplifying the positive effect of wealth changes on entrepreneurial entry by 0.65%. For households gaining wealth through investments, this effect is much lower, below 0.1%. These findings help explain the surge in business applications during COVID-19, driven by both credit tightening and lump-sum transfers.

Other work – please ask for draft through email

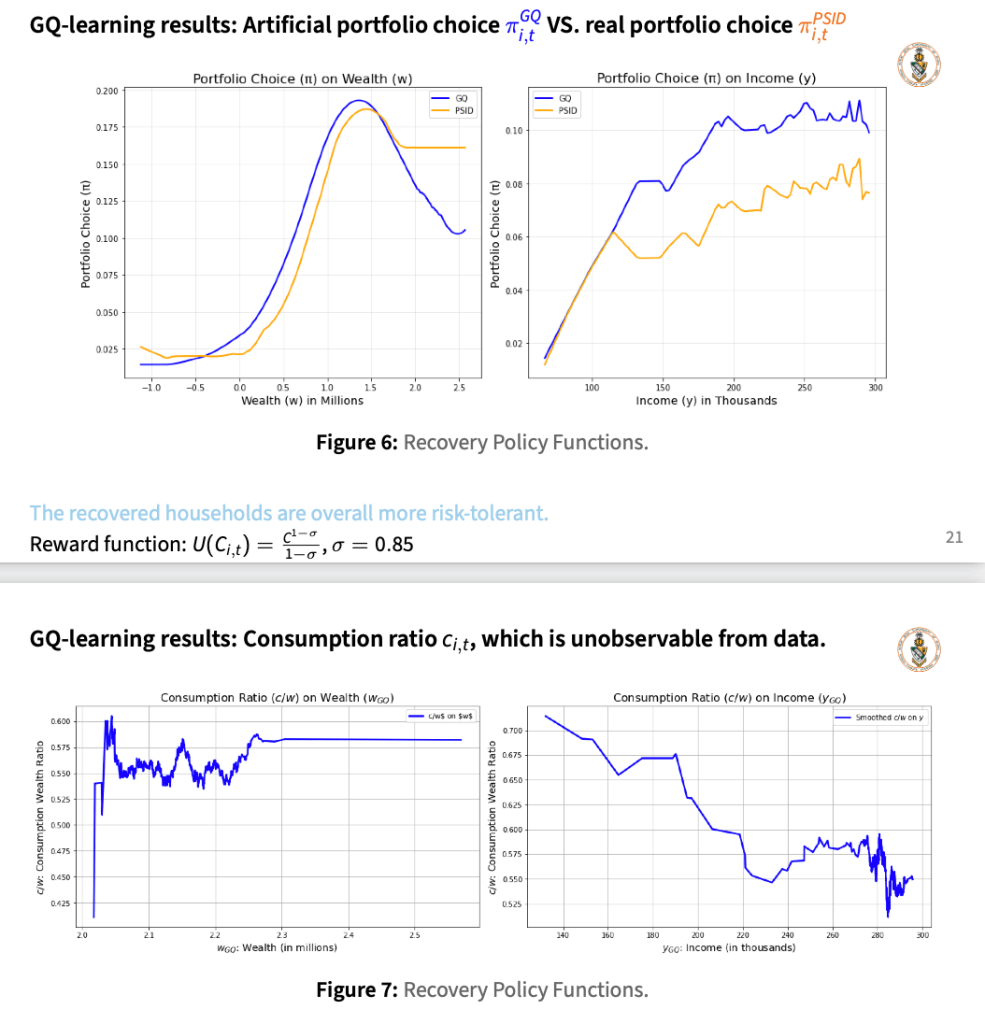

“Artificial Self-Insurance for Heterogeneous Households Using GQ-learning” [Slides] [Code] – Joint with Noah Williams

Scheduled for presentation on the 2025 Midwest Macro Meeting at Federal Reserve Bank of Kansas City.

Abstract

This paper introduces a novel approach for generating household-level decision rules by combining G-estimation with Reinforcement Learning. I demonstrate this method using the example of heterogeneous households’ portfolio choices in response to recessional income shocks. The method indirectly estimates the law of motion while accounting for the high-dimensional macroeconomic environment by treating these shocks as time-varying factors that affect households’ portfolio choices and consumption decisions differently. The Q-learning algorithm, a key Reinforcement Learning technique, is employed to recover agents’ choices at each time step. G-estimation then uses these recovered choices, shocks, and high-dimensional macroeconomic exogenous variables to predict subsequent state variables, guiding the learning of future decisions. This iterative process recovers all agent-specific state and key choice variables over time. We evaluate the algorithm by comparing the recovered choice variables with the decision rules of a theoretical economic model, using its simulated data. Finally, the algorithm is applied to real-world panel data, recovering the choice variables of households across the wealth distribution quintiles for the year 2009. We then examine how these households make consumption and investment decisions under the influence of recessional income shocks. We find that households in the 4th and 5th quintiles of the wealth distribution actively hedge against aggregate income shocks, while those in lower cohorts tend to reduce risky asset investments to stabilize consumption when the income index is at a lower level.

“Financial Constraints and Entrepreneurship in the U.S.” [Code]

Abstract

This paper addresses conflicting evidence on household credit constraints and entrepreneurship. While some studies indicate credit barriers for business startups, others suggest entrepreneurship prevalence only among wealthy households, implying there are little households financially constrained for starting businesses. This paper investigates the conflict in the literature regarding household credit constraints and entrepreneurship, examine their ability to accumulate “seed funds” through investing, and analyze how constraints affect business sustainability. Using two waves of COVID-19 stimulus checks as quasi-experimental income shocks, I explore their impact on credit constraints. Additionally, I employ a shift-share instrumental variable based on portfolio compositions, with lagged asset shares and macroeconomic asset price shocks, to assess aggregate asset returns’ impact on constraints. I demonstrate that shift-share instrumental variable assumptions hold under arbitrage pricing theory and common factors in asset pricing. My findings show credit constraint relaxation significantly encourages entrepreneurial entry for the 1st and 2nd wealth quintiles (on the wealth distribution of year 1999). Different sources of constraint relaxation (inheritance, fiscal transfers, collateral, or stock appreciation) affect business entry and retention differently across wealth quintiles. House price appreciation encourages business entry and retention for middle quintiles, while stock appreciation crowds out entrepreneurship for households above the 20th percentile of wealth distribution.

Woking in Process

- Signaling Innovation: The Role of Financing Channels